Machining Industry × Iran War — Second-Order Shock: Energy, Logistics & Margin Erosion — April 2026

Iran War Second-Order Industrial Shock: Energy, Freight & Predictability Risk for Machining, April 2026

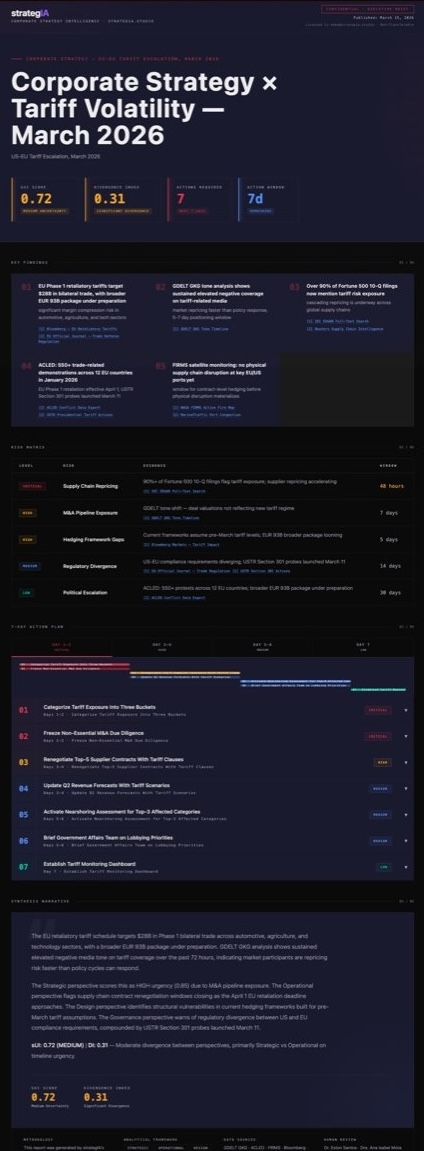

Executive Summary

For the machining sector, the war in Iran represents less an immediate risk of metal scarcity and more a combined shock of energy, logistics, and predictability — with direct effects on margins, lead times, and investment decisions. The Hormuz/geopolitical shock transmits into machining not through a physical absence of steel, but through a consistent chain reaction: oil and energy costs rise, freight and marine insurance premiums follow, industrial inflation spreads, and the result is pressure on margins, working capital, and the ability to quote confidently on fixed-price contracts.

This report assesses five assumptions validated for robustness against alternative scenarios and produces six prioritized actions for machining sector executives. The sUI Score of 0.68 (HIGH) reflects a real but selective risk environment: the threat is not a structural supply collapse, but a sustained erosion of operational predictability that hits hardest at companies with fixed-price contracts, imported inputs, energy-intensive processes, and customer portfolios concentrated in slower-moving industrial segments.

Top Key Findings

- The primary transmission channel is not steel — it is energy, freight, and insurance. A1 at 80% means the Hormuz-linked energy cost premium remains embedded through Q3 2026. For machining shops running CNC equipment, furnaces, and heat treatment, industrial electricity and gas costs are a direct vector of margin compression that has nothing to do with whether your steel is sourced domestically.

- Aluminum and globally sourced specialty alloys carry materially higher risk than domestic carbon steel. A4 at 65% reflects that light metals and specialty alloys react faster to Persian Gulf logistics disruptions. If your material mix is heavily weighted toward aluminum or imported specialty grades, your supply exposure is different in kind — and more urgent — than a shop running standard ferrous grades from domestic mills.

- Fixed-price contracts without price-adjustment clauses are the single biggest financial risk. A3 at 70% captures that margin compression on established fixed-price contracts is already materializing for companies that have not renegotiated. The risk is not future — it is current P&L.

Top Risk: Energy cost inflation (A2 at 75%) combined with fixed-price contract exposure (A3 at 70%) produces an operating environment where machining companies simultaneously experience higher input costs and lower ability to pass them through — a margin squeeze transmitted by the war even for shops with entirely domestic supply chains.

sUI Score: 0.68 (HIGH) — The machining sector faces a real but selective systemic second-order shock. Risk is not uniformly distributed: companies most exposed are those with energy-intensive processes, imported or Gulf-route-adjacent material inputs, fixed-price long-term contracts, and customer segments hit directly by macro slowdown.

6 actions validated for robustness against alternative scenarios inside.

What you'll get inside

Full Report Preview

Get the Full Report

6 prioritized actions with full context, adversarial stress-test warnings, risk matrix, key findings, and downloadable watermarked PDF.

R$ 2.999,00 per report — less than 1 hour of consultant time.

One-time purchase · Instant access · Watermarked PDF included

Executive-grade analysis with the sUI methodology behind every score.

Buying multiple reports? Subscribe from R$ 11.999,00 for continuous sector coverage.

Powered by strategIA's agent ensemble.