Oil & Energy × Iran War Disruption — March 2026

Strait of Hormuz Closure, Yuan Oil Settlement & Global Energy Supply Shock — Iran War, March 2026

Executive Summary

The February 28, 2026 US-Israel strikes on Iran have triggered the most severe simultaneous maritime energy disruption since the 1973 oil embargo. The Strait of Hormuz — through which 21% of global oil and 20% of global LNG transits — is effectively closed: Lloyd's underwriters have cancelled marine insurance outright, and Maersk has suspended all services. Houthi attacks have simultaneously closed the Bab el-Mandeb, forcing all non-military tanker traffic to reroute via the Cape of Good Hope, adding 10–14 days and over $1M in additional fuel costs per voyage. Iran's announcement of oil sales in yuan on March 12 adds a petrodollar dimension that energy trading desks are not yet fully pricing.

sUI Score: 0.66 (MEDIUM-HIGH) — Lower divergence than corporate or defense reports (DI: 0.24) reflects broad agreement on the severity of the supply disruption. Primary uncertainty is OPEC+ political decision-making on spare capacity (C7 at 45%) and Kharg Island damage extent (C6 at 50%).

7 validated for robustness against alternative scenarios actions inside. Each action references the probability assumptions that govern its urgency.

What you'll get inside

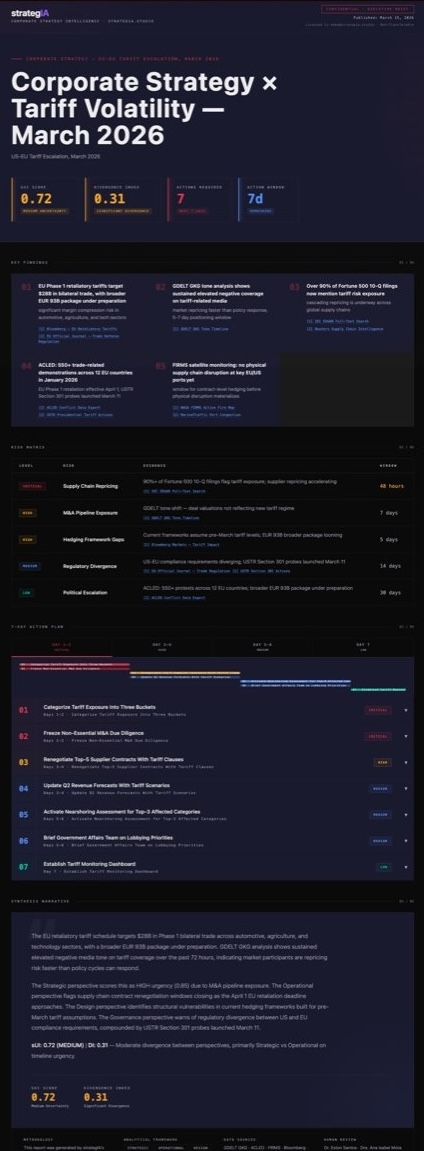

Full Report Preview

Get the Full Report

7 prioritized actions with full context, adversarial stress-test warnings, risk matrix, key findings, and downloadable watermarked PDF.

R$ 2.999,00 per report — less than 1 hour of consultant time.

One-time purchase · Instant access · Watermarked PDF included

Executive-grade analysis with the sUI methodology behind every score.

Buying multiple reports? Subscribe from R$ 11.999,00 for continuous sector coverage.

Powered by strategIA's agent ensemble.