Semiconductors & Electronics × China Rare Earth Weaponization — March 2026

China Rare Earth Export Suspension & Taiwan Strait Tension, March 2026

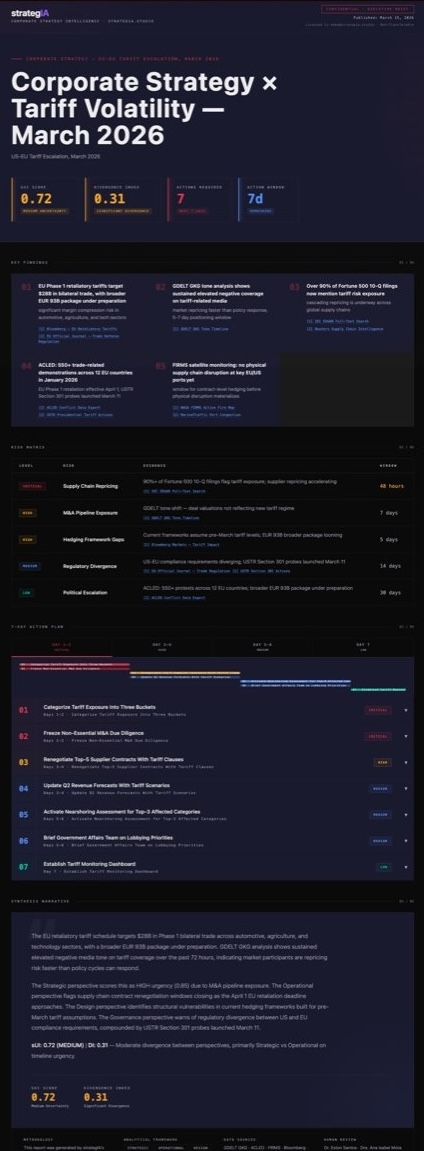

Executive Summary

China's suspension of rare earth exports — initiated in April 2025 for medium and heavy categories and extended in December 2025 to internationally-manufactured products using Chinese-origin materials — has fundamentally restructured the geopolitical risk profile of the global semiconductor and electronics supply chain. With China controlling 91% of rare earth separation and refining and 94% of permanent magnet production, the weaponization of critical mineral supply is no longer a theoretical risk scenario: it is the operating environment.

This report assesses six validated for robustness against alternative scenarios assumptions across the rare earth supply squeeze and Taiwan Strait escalation risk, producing seven prioritized actions for semiconductor and electronics executives with decision horizons ranging from 48 hours to 18 months. The sUI Score of 0.87 — the highest rating in this intelligence cycle — reflects a near-critical strategic uncertainty environment driven by simultaneous export control escalation and geopolitical military tension.

Top Key Findings

- The December 2025 third-country control expansion is the compliance trap most legal teams have not yet mapped. Products manufactured in Germany, Japan, or South Korea using Chinese-origin rare earth materials are now subject to Chinese export controls at the point of export from the country of manufacture — not just at the China border. This dramatically expands the number of companies with direct compliance exposure.

- Taiwan produces 85% of advanced AI chips globally, and a Taiwan Strait blockade scenario carries a 65% probability of material escalation within 12 months. This is above coin-flip probability. Any company that has not modeled the blockade scenario in its supply chain continuity plans is making a strategic bet — not a decision.

Top Risk: China's rare earth export suspension combined with the December 2025 third-country control expansion creates a near-certain production impact scenario (A1 at 90%, A2 at 85%) for any company that has not yet audited its full supply chain for Chinese-origin mineral exposure — including materials processed outside China.

SVI Score: 0.87 (HIGH) — The semiconductor sector is operating in the most volatile strategic environment since the 2010 rare earth crisis, with simultaneous supply weaponization and Taiwan Strait escalation risk compressing decision windows to 48-72 hours for the highest-priority actions.

7 validated for robustness against alternative scenarios actions inside.

What you'll get inside

Full Report Preview

Get the Full Report

7 prioritized actions with full context, adversarial stress-test warnings, risk matrix, key findings, and downloadable watermarked PDF.

R$ 2.999,00 per report — less than 1 hour of consultant time.

One-time purchase · Instant access · Watermarked PDF included

Executive-grade analysis with the sUI methodology behind every score.

Buying multiple reports? Subscribe from R$ 11.999,00 for continuous sector coverage.

Powered by strategIA's agent ensemble.